By Shannon Santschi

Most Americans are saving more money today than they did pre-pandemic. The St. Louis Federal Reserve Bank notes that from the end of the Great Recession (June 2009) to February 2020, “the personal saving rate has averaged 7.25%.” But since the pandemic, their research shows that the personal saving rate has shot up to 17.9%. This trend is definitely a move in the right direction, but is it enough?

The answer to that question depends on various factors, including age, prior savings, debt load, expected expenses, lifestyle, insurance coverage, and projected age of retirement. While we don’t have time to examine these variables in detail, know that most financial experts advise 1) having, at a minimum, a stash equivalent to three months of living expenses in an emergency fund, and 2) saving between 10-15% of your income on an annual basis.

If you know that you’re not on track with your savings or don’t have enough in your emergency fund, draft a plan today to reroute yourself.

Increasing your savings will be most effective (and more exciting) when you do the following simultaneously: 1) cut your spending and 2) increase your income.

Cut Your Spending

Knowledge is Empowering

Get an accurate picture of where you are spending your money by examining your bank account or credit card statement. Most banks and credit card companies now provide graphs that map by category where you spend most of your money. Common categories include: Housing, Church/Charitable Giving, Entertainment, Transportation, Groceries, etc.

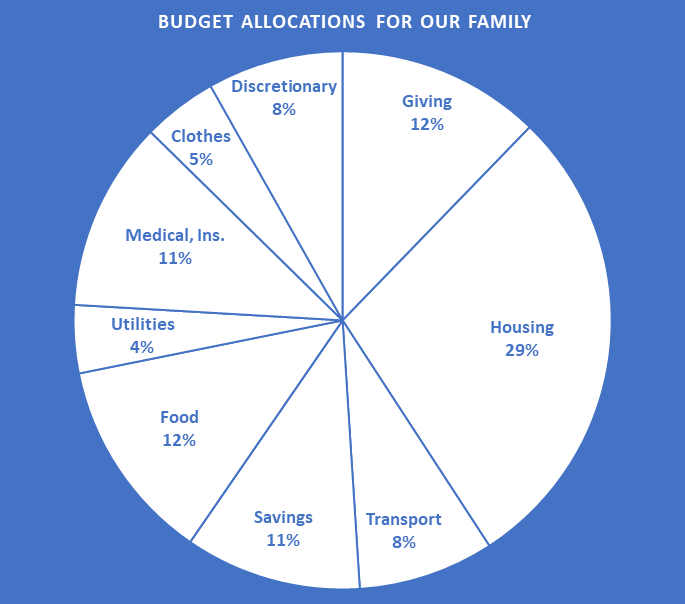

Financial experts make budget allocation recommendations to help consumers meet needs, some wants and avoid debt. In general, their allocation recommendations vary only by a few percentage points. (Check out this website for a fascinating peek at how the average American household allocates its budget.) Here’s a graphic of the ideal budget allocation I made for our family, using experts’ recommendations. I created it using Microsoft Word’s chart templates.

If your real-life expenses exceed your ideal budget allocations, you’ll hamper or even eliminate altogether, your ability to save and invest for the future. Do what it takes to bring your allocations into harmony with each other.

Increase Your Income

1. Get a side-gig doing something you enjoy (so it doesn’t feel like work) to bring in some extra cash.

2. Sell some of your stuff. Put the proceeds in savings.

3. If you are out of debt and have a little extra, invest it in an interest-bearing account that at the least beats inflation. Talk to your banker, credit union, or broker to figure out what’s suitable for you.

Strategies

Warren Buffet famously once said, “The chains of habit are too light to be felt until they are too heavy to be broken.” Saving money is not just hoarding cash. It is about developing attitudes and habits that make it easy to save and harder to spend. Take a look at the strategies below and test drive at least one today:

1. Use Cash More, Credit Cards Less – According to a study conducted by Dun & Bradstreet, people who use credit cards spend up to 18% more on purchases! Swiping a card is relatively inconsequential—we don’t experience the visual loss of money. Our brain focuses on the pile of goods in our cart. For most of us, paying in cash is a bit more painful. We instantly know what we’re giving up, which can cause us to be a bit more conservative in our spending.

2. Get Out of Credit Card Debt with Another Credit Card – See if you can transfer high balance, high-interest cards to a card that has a zero balance at a low interest rate. Often you can get a promotional rate that is 3% or less. The trick will be never to use that card until you pay off that debt completely.

3. Develop a Budget – Write it down, post it in a visible place. If you are single, get an accountability partner to help you stay on track.

4. Track every purchase using an app – Many personal expense tracker apps are free or available for a relatively low fee. You’ll be able to stay on top of how closely you’re sticking to your budget, better recognize subconscious habits, and realize opportunities to save by observing your analytics–often available in charts and graphs. Plus, you’ll feel like a boss as you practice being the CEO of your money. NerdWallet provides a nice overview of several popular budget apps.

5. Take a personal finance course – Stay humble so you can truly learn and change bad habits. Pro-tip: Hang out with like-minded people who are also actively working to save money and eliminate debt.

6. Get emotional about saving – Know your “why” for saving. A study commissioned by Capital One found that people who had a sentimental reason for saving, saved three times more than unemotional savers. For example, “I’m saving so I can surprise my husband with a trip to the Holy Land.”

7. Automate your savings – You won’t miss what you didn’t know you had. Schedule automatic withdrawals from your paycheck to a savings account. Increase the amount you’re saving by one percent at least once a year.

In sum, make this National Savings Day count by assessing your situation, drafting a vision of where you want to be in one year, and taking at least one action toward that vision today!

Shannon Santschi is a contributing writer for Smart Women Smart Money Magazine. Comments or questions can be sent to staff@smartwomensmartmoney.com.

{kind=link}